Swiss bank UBS expects a surprising development for the Greek economy in 2023, increasing its forecast for the GDP growth rate to 3% this year (from 2.5% previously) at a time when the average estimate of economists of international organizations and of analysts ranges at a meager 0.6% (against 1.2% by the commission).

The Greek economy, which closed 2022 as it estimated with a GDP growth rate in the region of 5% (against its initial estimate of 6.4%), will continue to grow at a strong rate, at 3.2% in 2024 as well.

The reasons for optimism

For UBS, there are several reasons for optimism for the Greek economy this year, as lower energy prices and thus lower subsidies are expected to reverse the large gap that opened between gross value added and GDP in the third quarter of 2022, favoring growth, while the drop in fuel, electricity and natural gas prices will also limit average inflation to 3.3% or 150 basis points below the average market estimate.

The above, combined with talks of a new 8%-9.5% increase in the minimum wage from April 1st, should lead to a rise in real wages which was not included in previous forecasts.

Also, last year’s primary fiscal deficit was 0.5-0.7% of GDP (better than the target of -1.7% of GDP), while lower energy subsidies and a better start to 2023 imply upside risks for this year’s projected primary surplus (+0.7% of GDP). Greater fiscal space allows for either faster debt reduction or additional support measures.

The predictions

At the same time, the forecasts for the growth of the eurozone for 2023 have been revised upwards by 60 basis points to 0.8%, which also points to a better macroeconomic scenario for Greece. With reference to the individual macroeconomic forecasts for 20223, it predicts GDP at 223 billion. euros, increase in private consumption by 3%, fixed capital investments by 15%, exports by 4%, imports by 5%.

It forecasts a primary surplus of 1% this year and 1.6% in 2024 and a fall in the debt ratio to 158.5% of GDP this year and 151% of GDP in 2024.

In the medium term, it predicts a de-escalation of inflation to 3.3% this year and to 2.2% in 2024.

Greek bonds

In the above environment, the positive outlook for Greek bonds also remains, despite the election cycle with the market adopting the strategy of markets in corrections at a time when the profile of Greek debt (maturity close to 20 years) stands out overall in the eurozone.

Also Fitch, DBRS and S&P are one step away from giving Greece an ‘investment grade’ rating, an upgrade could give a significant boost to Greek bonds.

It predicts that 10-year bond yields will decelerate to 3.5% at the end of 2023 and to 2.15% at the end of 2024.

At the same time, double-digit growth in corporate lending is expected, better-than-expected asset quality and a healthy capital structure from Greek banks, while higher interest rates are driving the sector to high single- to low-double-digit RoTE this year.

Higher profitability, mid-single digit NPL rates, stronger capitalization support Greek banks’ plans to return to dividend accommodation.

Elections

The Swiss bank also makes a special mention of the upcoming elections and after explaining that for the electoral system (simple proportional in the first ballot box and reinforced in the second which produces self-reliance with 38% of the votes), it observes that the average of the last five polls shows victory for New Democracy with 37.5% against SYRIZA’s 29.5% and PASOK’s 11.5%, which increases the chances even for New Democracy’s ability to form a government alone in the second round.

Latest News

Greek Government Reissues 10-Year Bond Auction for €200 Million

The amount to be auctioned will be up to 200 million euros, and the settlement date is set for Friday, April 25, 2025 (T+5)

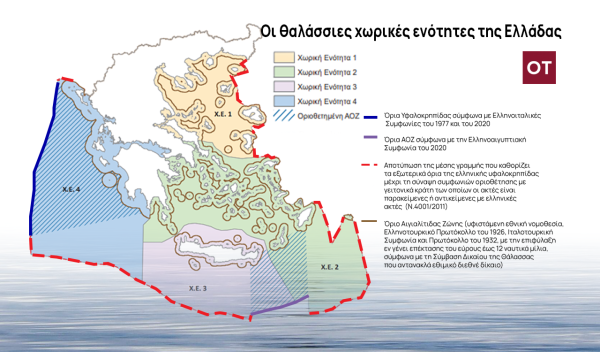

Greece Defines Continental Shelf Limits and Maritime Zones in Landmark EU Document

The Maritime Spatial Planning (MSP) framework represents a comprehensive approach to spatial planning and is crucial for the successful development of a blue and circular economy

EU Praises Greece’s RRF Progress as Revised Recovery Plan Nears Completion

Athens is preparing to submit its revised “Greece 2.0” Recovery and Resilience Plan after Easter, with a slight delay from the initial timeline but with the European Commission’s approval.

Greek €200M 10Y Bond to be Issued on April 16

The 3.875% fixed-interest-rate bond matures on March 12, 2029, and will be issued in dematerialized form. According to PDMA, the goal of the re-issuance is to meet investor demand and to enhance liquidity in the secondary bond market.

German Ambassador to Greece Talks Ukraine, Rise of Far Right & Tariffs at Delphi Economic Forum X

Commenting on the political developments in his country, the German Ambassador stressed that it was clear the rapid formation of a new government was imperative, as the expectations across Europe showed.

Athens to Return Confiscated License Plates Ahead of Easter Holiday

Cases involving court orders will also be excluded from this measure.

Servicers: How More Properties Could Enter the Greek Market

Buying or renting a home is out of reach for many in Greece. Servicers propose faster processes and incentives to boost property supply and ease the housing crisis.

Greek Easter 2025: Price Hikes on Lamb, Eggs & Sweets

According to the Greek Consumers’ Institute, hosting an Easter dinner for eight now costs approximately €361.95 — an increase of €11 compared to 2024.

FM Gerapetritis Calls for Unified EU Response to Global Crises at EU Council

"Europe is navigating through unprecedented crises — wars, humanitarian disasters, climate emergencies," he stated.

Holy Week Store Hours in Greece

Retail stores across Greece are now operating on extended holiday hours for Holy Week, following their Sunday opening on April 13. The move aims to accommodate consumers ahead of Easter, but merchants remain cautious amid sluggish market activity.